MIPS AB – Helmet Safety Monopoly with No Worthy Rivals

MIPS AB – Helmet Safety Monopoly with No Worthy Rivals

MIPS is the industry standard for helmet safety - a unique business with durable technology and scale advantage, potentially a compounding machine.

Hi, my fellow Sleep Well Investors (SWIs),

I am Trung. I write 10+K words deep-dives on market leaders. I also write Thesis Trackers updates to follow up on their performance. When the right price comes, I buy them for the Sleep Well Portfolio, which I am building for my 4-year-old daughter to redeem in 2037. I disclose the reasoning of all BUY and SELL (ideally never) transactions (1st, 2nd, and 3rd). Join me in building generational wealth.

Introduction

MIPS AB (MIPS.ST, listed on the Stockholm Stock Exchange) is a pioneer and market leader in helmet safety systems for bicycles and adventurous sports, including skiing and equestrian.

Short for Multi-directional Impact Protection System, it’s a low friction layer between the helmet foam and the helmet liner, allowing for a sliding motion of 10 to 15mm in all directions. The core technology was invented 25 years ago in Taby, Sweden, to reduce the risk of brain injuries from accidents involving rotational collisions. It was considered a leap from the old ways that only protected users from linear impacts or straight-on collisions.

Today, it is the most recognizable brand in the industry. The small yellow dot logo on the outside of the helmet, and the yellow liner MIPS, represent ‘increased safety’ and are considered the standard for the industry.

Since launching the first helmet for horse riding in 2007, it has dominated every market it has entered, namely, road bikes, mountain bikes, and snow sports. 91 of the top 100 highest-rated helmets use MIPS technology. The first non-MIPS position is at 30th place (!). Over 200 brands, including 9 of the top 10 bike brands and 6 of 6 biggest snow sports brands, are MIPS customers. For example, Specialized, Alpina, Fox, and Poc. The next competitor has just two brands as customers (!)

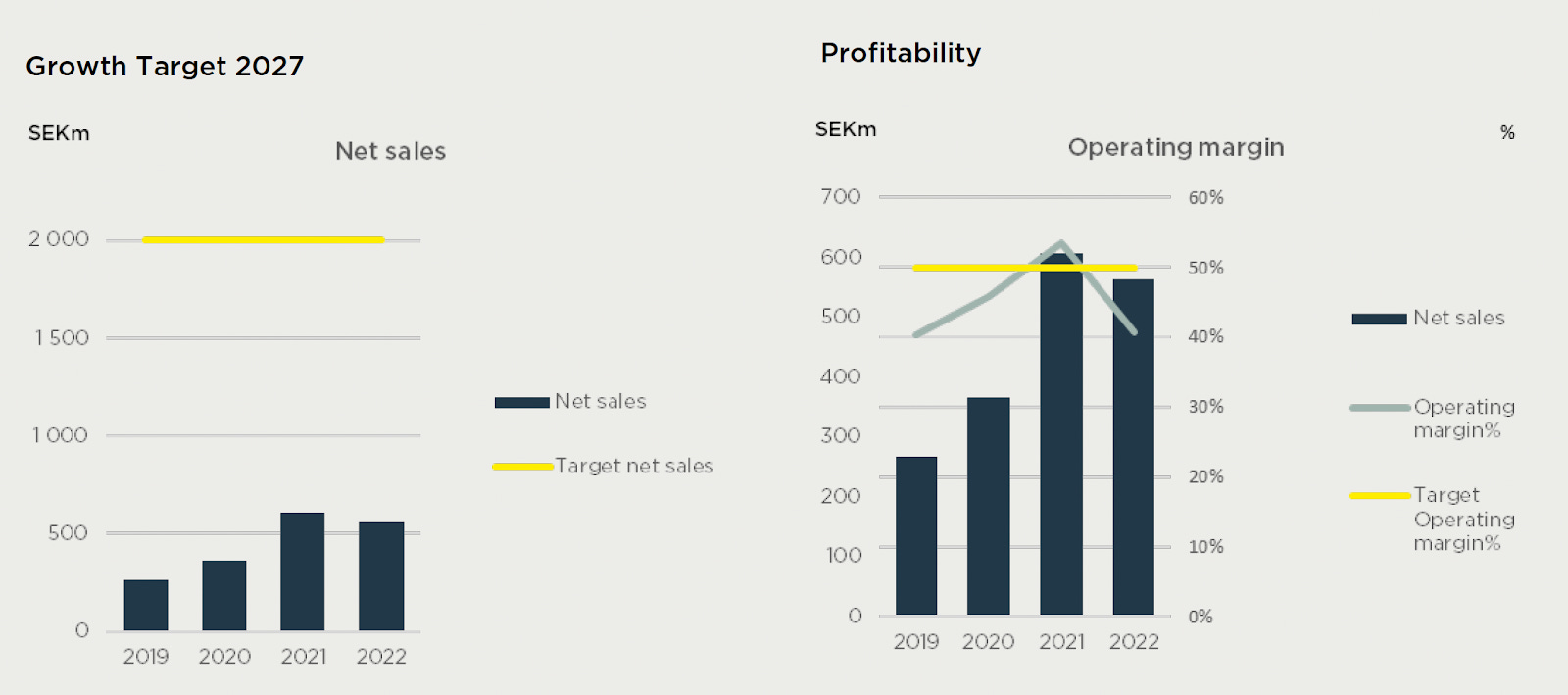

MIPS has compounded revenue by 49% CAGR, earnings by 62% CAGR, and free cash flow per share by 39% CAGR since 2014. The gross margin has remained over 70% since 2015, and the EBIT margin has stayed over 38% since 2018, showing strong pricing power and market dominance.

There is no doubt MIPS has benefited from the Covid bike-craze demand-pull and is now suffering from a bloated bike market. Sales fell by 46% YoY in Q4’22 and 7% YoY for FY22. However, before investors conclude that this is a Covid business, know that MIPS’s revenue per share compounded by 62% pre-covid from 2014 to 2019.

MIPS’s leadership position will likely be unchallenged as it possesses multiple durable moats. Among them is the growing portfolio of 300 long-dated patents in over 40 families (including energy absorption layer and sliding facilitator), scope and depth of tests conducted over two decades with third-party validations, unrivaled distribution scale afforded by a clever business model, agnostic design of the safety component, and strong relationships with practically all helmet makers from the beginning of its product launch.

Interestingly, one of the top bike producers was MIPS’s largest investor in the early days. Lastly, MIPS's impressive 35%+ return on capital invested (ROIC) means that as it enters the motor and safety (workplace / industrial / defense) markets, the business can replicate the effective investment process to keep compounding and delivering value to all stakeholders.

With large untapped markets, the management aims to triple its annual revenue to SEK 2B and expand its EBIT margin to over 50% by 2027, an upgrade from SEK 1B and a 45% EBIT target by 2025 set in 2021.

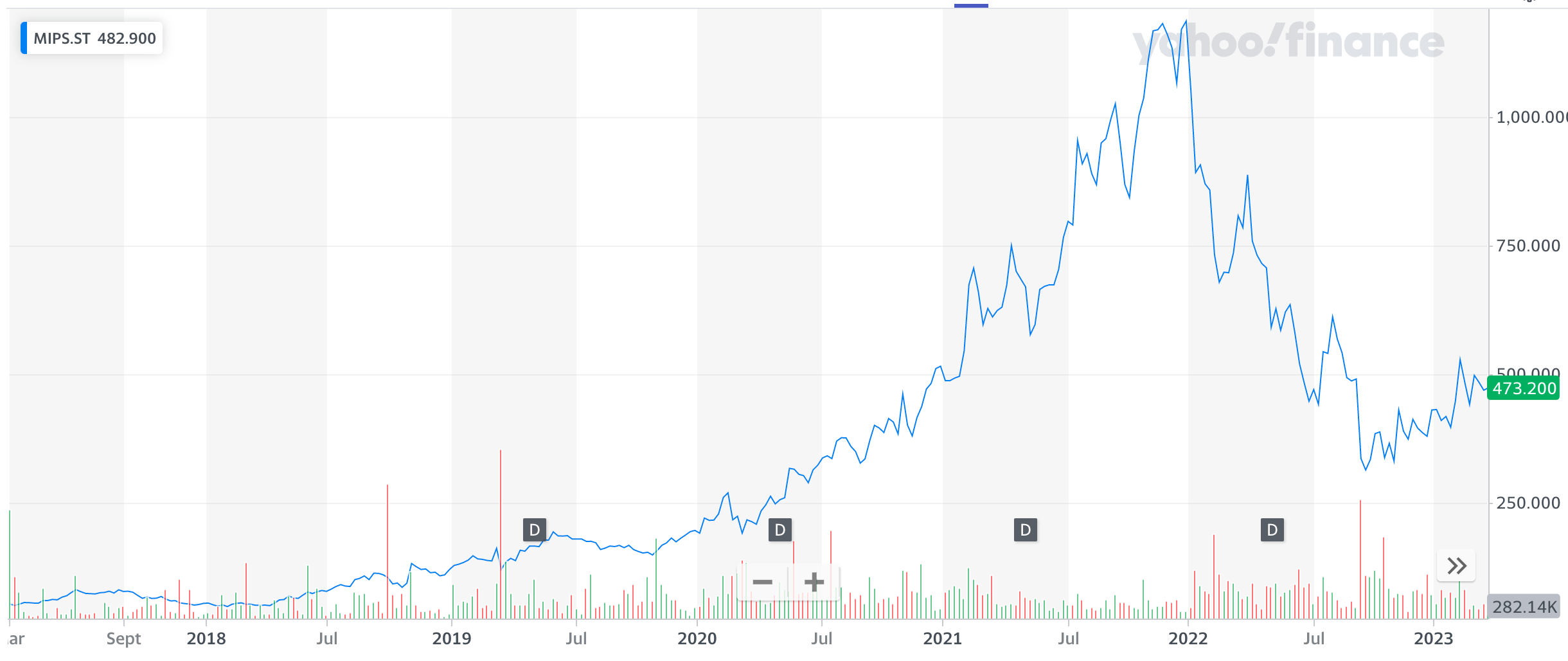

MIPS’s stock had returned 9x to shareholders, compounded 38% CAGR since its IPO in 2017 when it was at ~SEK 2B Market Cap, ~SEK 50/share, to the current value of ~SEK 12B Market Cap, or SEK 470/share, despite crashing 60% from the peak of ~SEK 33B Market Cap, ~SEK 1250/share.

The current twelve-month trailing multiples are at 55x PE and 70x FCF. This appears expensive on an absolute level but undervalued relative to historical levels, the uniqueness and dominance of the business, the size and trajectory of its moats, and growth potential. My DCF workings also confirm the stock is modestly undervalued at the base case and potentially attractively priced if inventory issues digest faster (we will track this).

Readers of Sleep Well Investments know I aim to own only time-tested businesses that can endure competition and turbulence.

The VAT Group - Vacuum Valve Monopoly (thrived since 1965)

Floor and Decor - Hard-surface Flooring Future Monopoly (2001)

MIPS is relatively less tested than my previous ideas. However, it makes up for an enviable market position like Shimano and low competition threats like The VAT Group.

Competitors with a similar business model and technology effectiveness are limited to only a few brands, and the own-branded solutions are not a threat. Additionally, customers (helmet makers) are not incentivized to compete as the cost of the component is low, and the technology barrier to entry is high.

My research into each competitor found they lag far behind MIPS regarding test data, scope and depth of patents, distribution scale, and customers' and users’ mindshare. Moreover, as the market is unlikely to change (since bicycle helmets ever existed, it has changed only once from protecting against direct impact to angled/oblique impacts), MIPS should retain the industry standard helmet safety status. It should also gain market share in adjacent (motorcycle and safety) markets in the next 10 to 20 years.

The setup provides an attractive long-term investment whereby valuation plays a lesser role as long as the business continues to compound and management keeps their eyes on the ball (I’ll be keeping a close tap on management’s execution).

The bottom line is that you are investing in an industry leader that is already cash-rich, highly profitable, and expected to grow its revenue and earnings at high double digits in a conservative scenario. As a result, the downside is limited, and the risk/reward warrants an eventual 3% position in my portfolio.

*Disclosure: MIPS is a 1% position of my portfolio, Shimano 3%, FND 1.5%, and VAT 1.5%.

Below is what you can expect in the analysis:

Why is MIPS a sleep-well business?

Setting the industry standard - irreplaceability

Ingredient brand business model - scalability

Financial fortitude - growing profitably

Capital allocation - compounding value

Long-term and ambitious management

How does MIPS overcome competition and other threats?

Competition (KASK, LEAT, SPIN, WaveCel, and others)

Durable moats (Brand / Technology, Scale/cost, Switching cost)

Key risks

Valuation - what is the right purchase price?

Base case

Bear case

Bull case

Sleep Well Investments scorecard